Co-authored by Fraser Edwards and Javed Khattak

Every so often, we are asked why Self-Sovereign Identity (SSI) needs a token. Originally we expected the explanation of “why” to be a long piece but a recent experience provided the material for a much shorter, practical blog.

Usually the question of “why does SSI need a token”, stems from people’s belief that there are existing, viable payment rails. As Sovrin outlined in their whitepaper back in 2018, traditional rails don’t work when issuers and receivers of @credentials are unlikely to have a direct contractual relationship since the user is at the center with SSI.

Since then, the crypto world has moved on massively with respect to tokens but especially in the area of stablecoins.

Stablecoins: Take your pick

Which brings us neatly onto two contrasting examples we have experienced at cheqd recently.

Example

We work with multiple law firms for their different areas of expertise, but for this, I’ll be focusing on just two of them (obviously anonymously):

- cheqd can pay via both USD and USD Coin (USDC) and holds accounts in country A and country B.

- Firm A takes payment in USD. Their bank is based in country B but they use an intermediary bank in country C.

- Firm B takes payment in USDC.

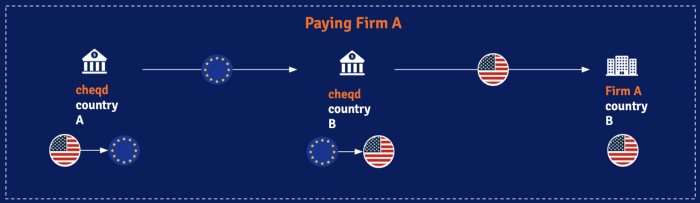

Firm A

To pay Firm A, we had a period of a week checking whether we could send directly from our bank account in country A where we hold the bulk of our funds to Firm A’s account in country B. Paying directly from our account in country A is our preferred option since we get good exchange rates.

Unfortunately, we couldn’t send this payment via USD and hence had to begin checking losses from exchange rates and fees to make sure we got the amount right and minimise our losses. Eventually we landed on sending the payment in multiple-steps, from our account in country A to our account in country B which required USD to EUR conversion due to the network used for the overseas transfer requiring EUR for the transfer. This was then converted back into USD due to Firm A’s invoice being in USD, and only then on to the Firm’s account in Country B.

A hop, skip and a jump all to make one simple payment

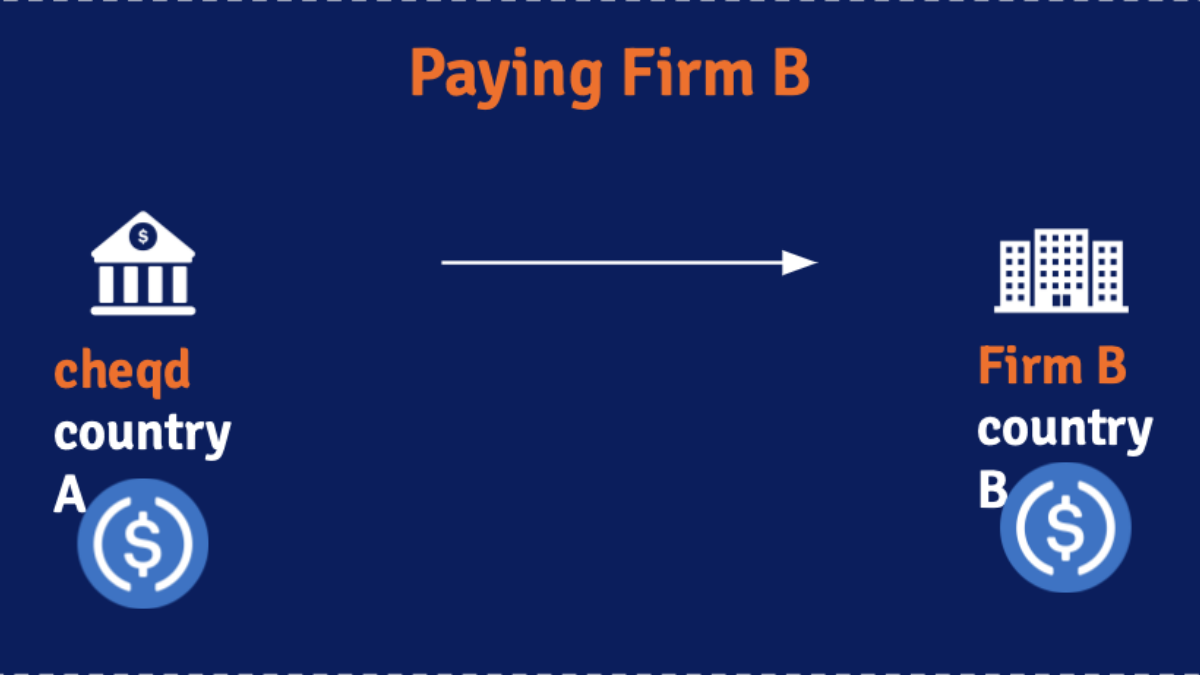

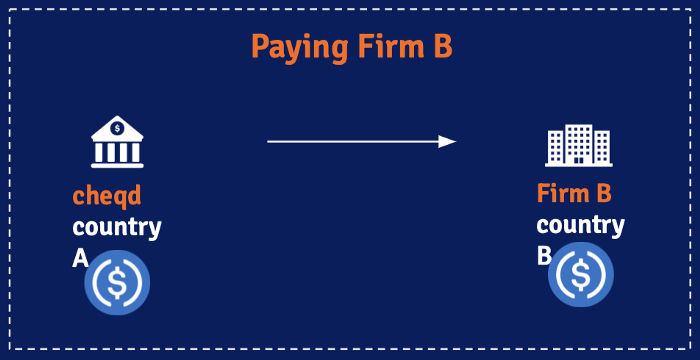

Firm B

Barely worth a diagram

So what?

Even where companies have contractual relationships, settling payments is still a huge headache. Whilst this example has been slightly extreme, we’re sure it won’t be the last time we experience it. The difference between the two experiences can be seen purely from the number of lines written. Multiplying these by hours and days then shows the opportunity lost elsewhere in the business.

From this example alone, expecting payments across an SSI ecosystem to be seamless and scalable using existing payment rails is laughable. As other industries and technologies from finance to distributed storage like IPFS and Filecoin, SSI needs to embrace tokens to be truly successful.

The marketing benefits

Less considered is the marketing benefit a token could have for SSI. Whilst companies are beginning to wake up to the possibilities, there is very little awareness amongst the general public. SSI has a tremendous community of passionate believers but it has not cracked the public consciousness yet or broken materially out of the core supporters who have typically worked in the identity space previously.

A token provides a massive opportunity to broaden the audience. As a recent applicant said in an interview with us:

“My Dad can’t switch on his computer but comes downstairs telling me about bitcoin market movements”

Wouldn’t it be wonderful for discussions on SSI to be everywhere?

Building public awareness will be key to having them drive adoption, and once they have experienced SSI in any area of their lives they will demand it of any organisation they interact with. The parallels with neo-banks and the incumbent banks are strong here. Most neobanks restructured their Know Your Customer (KYC) processes, moving from users filling in endless forms to be checked by an analyst to scanning identity documents, leveraging credit agency databases and taking quick selfies. This allowed them to provide KYC journeys in the order of minutes rather than days. That journey is now pervasive not just across banking but also car rental to coworking spaces amongst others.

SSI will be the same, once someone experiences SSI, they will demand it of all their interactions.

As important, a token will provide a mechanism to being rewarded as the technology is adopted. There won’t just be rewards in terms of user experience and reclaiming privacy but also monetary rewards for supporting the ecosystem and encouraging adoption.

Key takeaways

A token is sorely needed to enable SSI to truly grow. Existing payment rails are not fit for purpose, especially at global scale. It will also help SSI break into the public consciousness and further drive adoption.

Thankfully, we at cheqd are building exactly this!

We would love to know your thoughts as always either as comments on the article or via any of our other channels below, take your pick! Make sure to join our rapidly growing Telegram community here to stay updated with our latest news as we head towards launch.

P.S. We’re also on Twitter or LinkedIn, make sure to “cheq” in!